Double-entry accounting is the standard for bookkeeping used by most businesses today. This accounting system gets its name because each transaction has two parts that record the source and destination of the funds. This minimizes errors, eliminates the need for duplicate transactions, and increases the chances that your books balance. Although the double-entry accounting system is best practice, some companies prefer to use the single-entry system. Today, we’ll compare the two systems and show how double-entry accounting works.

Shortfalls of Single-Entry Accounting

As its name suggests, the single-entry accounting method records each transaction once in each of the accounts affected by the transaction. So instead of creating one entry per transaction in the double-entry method, under the single-entry system, you’re required to create a minimum of two entries for a single transaction. The more complicated the transaction (i.e., the more accounts affected), the more entries you’ll have to create.

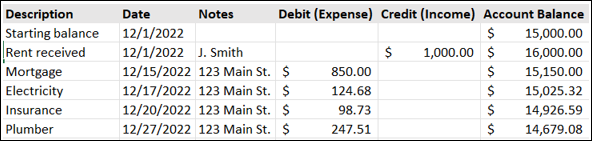

In the single-entry accounting system, all transactions are recorded in a cash book. This is a journal with columns for transaction details like dates, descriptions, whether a transaction is an expense or income, and the running balance. If you use a spreadsheet to track your expenses, you’re using the single-entry method, and your spreadsheet acts as your cash book. The example here shows the activity for the operating account for one property. It looks like a quick, easy way to track the activity, but remember that each account you want to track must have its own ledger or spreadsheet. The more information you want to track, the more spreadsheets you’ll have to maintain. Each bank account, income account, and expense account will have its own spreadsheet.

Even though single-entry bookkeeping might sound like the more efficient and easiest approach to bookkeeping, some accountants describe the single-entry method as an incomplete financial system because it only focuses on recording the bare essentials: revenue and expenses. Single-entry accounting doesn’t track liabilities and assets. If a property owner takes out a loan to cover renovation costs, under the single-entry system, the funds from the loan are recorded as income, because that’s the only option. In the double-entry system, those funds would be recorded as a liability, so the property owner could monitor the balance of the loan.

The single-entry system is more prone to bookkeeping errors and fraud than double-entry because, unlike in the double-entry system, there isn’t a way to balance each transaction. Without that failsafe, it’s easier to miss errors and carry them forward to the next accounting period. Think about a journal entry for a property purchase. In REI Hub’s sample journal entry for a newly purchased property, there are thirteen accounts affected. With the double-entry method, you can handle the purchase with one entry and easily ensure the debits and credits balance, so you’re not introducing errors into any accounts. But with the single-entry method, each account affected by the property purchase must have its own entry. That’s twelve more opportunities to record a figure incorrectly, and since the entries are separate, it will take significantly longer to track down where the error happened. Unlike double-entry accounting, single-entry accounting doesn’t provide a method to check for errors, so it’s easy to carry those errors forward to the next period.

Because the single-entry system doesn’t allow for liability balances or asset tracking, businesses using this accounting method aren’t able to produce balance sheets. Without a balance sheet, it’s harder to track liabilities and assets, so most companies using the single-entry system must track those items separately. Transactions that cross accounting periods also cause problems in the single-entry system since a service may be provided in one month but not paid for until the following month.

Advantages of Double-Entry Accounting

In the double-entry accounting system, each transaction has two parts: a debit and a credit. The debits and credits are recorded to different accounts and must balance, which acts as a double check and improves accuracy. The double-entry system tracks five types of accounts in your chart of accounts: assets, liabilities, equities, revenue, and expenses. Because this system records each transaction type, it’s comprehensive and lets businesses produce balance sheets, track inventory, and easily balance accounts, even when transactions cross accounting periods.

How Double-Entry Accounting Works

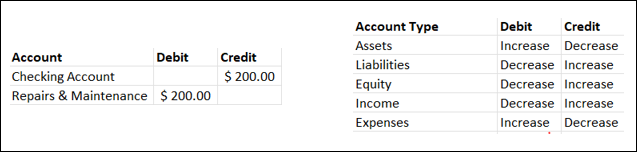

Let’s look at the double-entry system in action. If you hire an electrician to make a $200 repair at your rental property, the bookkeeping entry would look like this:

In the double-entry accounting system, debits are always on the left, and credits are always on the right. The type of account determines whether a debit or credit increases or decreases the account.

Each transaction will have at least one debit and one credit. The entry will affect only the accounts included in the transaction—in this case, the checking (asset account) and repairs and maintenance accounts (expense account). So this transaction will affect both the balance sheet and the profit and loss statement. The balance in your checking account shown on the balance sheet decreases by $200, and the repairs and maintenance line on your P&L report increases by $200.

Your books stay balanced because the change in your asset account matches the change in your expense account. This is a simple example, but balancing accounting entries gets tricky when multiple accounts are affected. Remember the property purchase journal entry? It had thirteen lines—plenty of opportunities to miss a digit or reverse two numbers. With the double-entry accounting method, you know the transaction balances because the debits and credits must be equal. In your REI Hub account, your transaction must balance before you can save it, that way you can’t accidentally introduce an error into your books.

What does a net positive or negative cash flow tell us?

When a company’s net cash flow is positive, the company has more money coming in than going out during that reporting period. The company has enough cash to fund its operations, pay off debts, and grow the business. But positive cash flow is not the same as being profitable. A business can be profitable without having a positive cash flow.

If the net cash flow is negative, the company isn’t generating enough cash to cover its expenses during that reporting period. However, cash flow differs from profit, so a negative cash flow statement doesn’t necessarily indicate a problem. For example, if an owner takes distributions out of the business, they’ll reduce cash flow. Or when a business expands, its cash flow may suffer in the short term, but as the expansion pays off, the cash flow should improve. Comparing the changes in cash flow from one statement to the next provides investors with a better sense of how the company is performing. Ideally, a company’s cash flow from its operating income should be greater than its net income.

Takeaways

Single-entry accounting sounds simple, but it doesn’t provide a full financial picture for business owners, and it’s easier for errors to slip through unnoticed. Double-entry accounting is a more complex system because it relies on your knowledge of various accounting principles and standards. However, its basis on logic and its built-in checks and balances make the double-entry accounting method user friendly. Because the double-entry system is comprehensive, it gives business owners a clear picture of their companies’ financial health at any point in time. REIHub makes double-entry accounting easy for rental property owners. Our transaction templates are based on sound double-entry accounting principles so you can save time and be confident in the accuracy of your property’s accounting reports.